I am often asked “In what markets do Hurst Cycles work best?”

I have always answered that Hurst Cycles work equally well in any liquid, well-traded market. But I now qualify that statement, by adding: ” … to the extent that it is not being manipulated”. The word manipulation generally has a negative implication, and so let me clarify that by manipulation I mean “any attempt to influence” … it is not necessarily a negative or evil manipulation!

I think this concept is a very important one to consider now as we are seeing more and more examples of (more and more complex) manipulation in the markets we trade.

When the European Central Bank announced its fairly extraordinary Quantitative Easing program this week, I started wondering what effect this would have on the markets, if any.

If you have been reading my market thoughts for any time you have probably realized that I am a fairly steadfast technical analyst in that I believe in trading the markets on the basis of a cycle analysis, a technical consideration as opposed to a fundamental consideration, such as news events, or bank actions like QE.

But this certainly doesn’t mean that I reject the idea that fundamental actions affect the markets. Of course they do, but the effect is usually either a temporary one, such as a strong move which is quickly retraced, or what I would call a coincidental one, where the fundamental action proves to be the trigger for an expected turn in the markets.

However manipulation over a period of time has a different effect on the markets. It serves to distort them.

And so I do expect the ECB’s QE plan to have an effect on the markets, but I don’t expect it to have the effect of prolonging the bull market indefinitely. In fact I don’t expect it to have much of an effect on the direction of European stock markets generally. (For a good quick explanation of the intended effect of QE take a look at the video here).

It is interesting that Europe is entering a phase of quantitative easing just as the US has ended their QE process. Did it have the desired effect in the US? Opinions are mixed about that, but the point that I would like to make in this post is that while the exact result of Europe’s QE process might be unclear, it will definitely have an effect on the markets. And that effect is one that particularly concerns us Hurstonians.

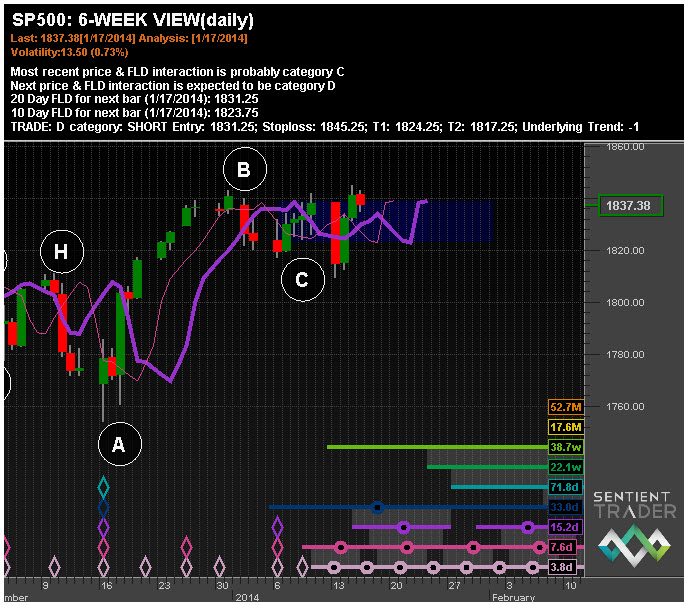

A divergence between the European and the US markets started developing recently, and I discussed this in my latest Hurst Trading Room podcast. I believe that the divergence is caused by the fact that the US markets are a bit further along in the current 54-month cycle than the European markets. Here is the S&P 500:

And the DAX:

Looking at those charts can we honestly say that we can see the effects of QE in the US? I think that perhaps we can, but not in the way that most people would expect. The big trough in March 2009 was not an effect of QE in my opinion, nor were any of the other peaks or troughs.

The effect that I think we can see is in a distortion of the cycles in the market. This distortion is often difficult to “see”, but it does have a dramatic effect on our analysis and trading of the cycles.

I am suggesting that any manipulation of a financial market (and QE is a manipulation in that it is an “attempt to influence”) does not succeed in changing the fundamental cycle structure of that market, but it does distort the market, making it more difficult to trade from a cycle perspective.

Any manipulation of a financial market does

NOT succeed in changing the fundamental cycle structure of that market,

but it DOES distort the market, making it more difficult to trade from a cycle perspective

In other words if financial markets were completely “free” (a Utopian and impossible idea I know, and before you think that I’m developing radical ideas I hasten to assure you that I am not proposing any sort of “free the markets” campaign!). If they were “free” and not subject to any form of manipulation then I think we would see very clear cycles, and trading those cycles would be a much simpler affair.

I also think that all markets experience varying degrees of manipulation at different times, and a corollary of my suggestion above is that the success of trading any financial market on the basis of a Hurst Cycles analysis is inversely proportional to the amount of manipulation that market is being subjected to.

A Practical Demonstration

I have an excellent demonstration of this principle which is also newsworthy at the moment: it is a practical demonstration of how the Swiss National Bank’s “pegging” of the Swiss Franc to the Euro affected trading the cycles in that market.

In June of 2014 I completed some hypothetical testing for a private fund manager. We were applying a Hurst Cycles “angle” onto an intraday forex trading system. I ran tests on many forex pairs and the application of a Hurst Cycles analysis consistently improved the trading performance on all pairs except for those that included the Swiss Franc (USDCHF, GBPCHF, EURCHF, even CHFJPY).

EDIT: I have received a few emails asking for some clarity about these tests, and so here is a little extra detail:

Let me tell the story with some pictures. The tests were performed on 15-minute bars over a period from 21 April 2014 until 19 June 2014. Here is a chart of the GBPUSD price movement over that time:

And the results of trading as shown by this equity line:

The x-axis is the number of trades, and the y-axis is the equity of the account. You can see a fairly consistent upward bias over the 290 or so trades.

Now here is the price movement of the EURCHF over the same period:

At first glance there is not a great difference between the price movements. In both there is the evidence of cycle action. Perhaps a little more “noise” in the EURCHF. Here is the equity curve in the EURCHF:

The contrast was stark, and at first I couldn’t understand it. I tried working with synchronized peaks instead of troughs, using the initial cyclic model instead of the default nominal model … nothing worked.

The conclusion I drew at the time was that because the Swiss Franc was pegged to the Euro, trading Hurst Cycles simply didn’t work. Of course there might be another explanation, and I would love to hear what you think.

I hope this example demonstrates the point that I want to make: manipulation of a market makes trading that market more difficult.

Conclusion

And so in conclusion, although I do not expect the ECB’s QE plan to change the overall direction of the European stock markets (which are destined to form a major trough within the next three years), I do expect that the QE plan is going to make trading those markets from a Hurst Cycle perspective more difficult.

6 thoughts on “Markets And Manipulation”

Hi David,

You raised some interesting points.

Firstly, as to which markets “Hurst cycles work best”, it has been my observation over the years that the US indices exhibit the most consistent cyclical behavior. It also depends on one’s definition of what constitutes a “Hurst cycle.” I apply the approach that the cyclicality is intrinsic in the price action and can be extracted with some of those “messy” calculations to which you referred. I’ve tested Hurst’s nominal spectral model over a 140 years of data and it is amazingly consistent. The one aspect of Hurst’s model that most spectral analysts overlook, but in my opinion is crucial to the accurate phasing of the price waves, is the taking into account the effect of the sideband modulation.

Secondly, the notion of market manipulation (quantitative easing, etc.) is, or should, be irrelevant to the cyclical trader. It is fundamental in nature and therefore is neither cyclical nor periodic. It is part of the long term underlying trend (four year wave dominancy envelope centerline or sigma L) and should be subtracted from the price action before a cyclical analysis is performed.

Lastly, the difficulty of applying Hurst cycles to the forex market is somewhat subtle. The easy answer is that forex exhibits much greater modulation than the stock market indices. This can sometimes wreak havoc on an approach employing Hurst’s trough synchronized, simple harmonic relationship model. The more subtle aspect is the nature of the base currency/quote currency relationship. A peak of the base currency is a trough of the quote currency. This runs afoul of the Hurst principle of always phasing waves to the price lows. It is most acute in the EURUSD pair since the quote currency (USD) can be traded separately (dollar index). The EURUSD is approximately 57% of the dollar index which causes it to exhibit a perfect inverse relationship (in terms of timing) to the dollar index. This causes the dominant waves (from a spectral viewpoint) to sometimes phase to the price highs and other times phase to the price lows. Fortunately this effect is not as pronounced on the very short, trading waves.

William

Hi William. The concept of whether to use synchronized troughs or peaks in forex is a fascinating one. As you say it seems to shift from one to the other at different times.

David, you should run the tests above on the CHF pairs again now the peg has been removed. That might provide some compelling reading!

My opinion is that these ‘manipulations’ are inherent in the cycles themselves, they are one catalyst to move price. It brings us into the realm of asking how do cycles form, where do they come from? If they are formed by cycles of human sentiment are these manipulations just an example of a desperate attempt, in this instance, to maintain the status quo by central banks, under the influence of a very large cycle in sentiment?Exactly the same as a naive investor holding onto a rallying stock on a 5 minute timeframe, hoping to make more and more gains. Eventually value is exhausted and price discovery must take over.

As we saw with the SNB the pressure builds and eventually breaks, snapping the cycle back to ‘balance’. After all, cycles never disappear, according to Hurst….

The DAX over the past two weeks has been clearly distorted in my opinion. There are cycles similar in time to all the other markets but they have been bent upwards. On a longer timescale this could look like a ‘temporary’ spike, referred to above, it all comes down to your frame of reference!

Hi David. I will definitely be looking at the Swiss Franc again, but it will take a while for there to be enough “clean” data to do a good analysis.

Hi David,

Your analysis of EURCHF is insightful and quite valuable. At the risk of sounding naive and/or a little provocative, I was wondering if you considered trading the inverse signal in EURCHF.

A model that delivers consistent losses over time is just as valuable as a profitable one, providing you take the opposite position.

Best regards,

Cedric

Hi Cedric. Yes indeed I did look at “inverting” the trading process, but it didn’t work very well. Those charts show the results after trading costs (and some slippage), and so when the trading process was inverted the equity did not increase as much as it had decreased on the original system. It did produce a marginally profitable system in theory, but the trading process involved taking a limited risk with a stoploss. Inverting the system meant taking theoretically unlimited risk, and limiting the profit. This combined with the fact that it was only marginally profitable meant that we rejected trading all the Swiss Franc pairs. Something that I am relieved about now!